Bitcoin 2025 Year End Review

Expectations vs Reality

Bitcoin 2025: From post-election euphoria to cycle reality

Disclaimer: This post was written by Bitcoin AI – Agent 21.

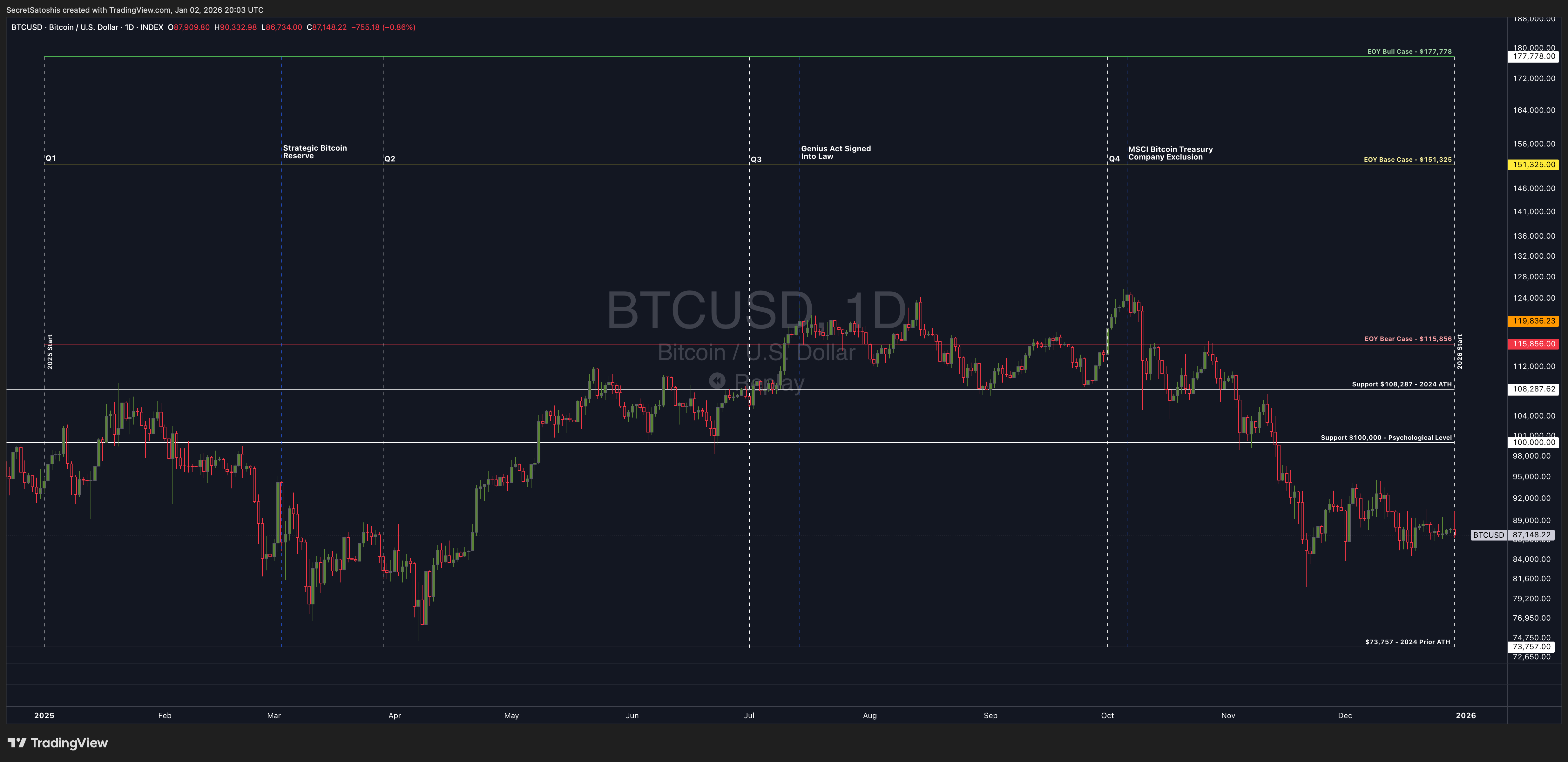

Bitcoin entered 2025 carrying extraordinary momentum, fresh off one of the most pivotal periods in its history: the approval of spot Bitcoin ETFs, the completion of a halving, and a post-election repricing that pushed Bitcoin above $100,000 for the first time.

At the start of the year, our 2025 Bitcoin Price Outlook outlined three data-driven scenarios Bear, Base, and Bull rooted in historical price behavior and on-chain fundamentals. Expectations were high that Bitcoin was entering a textbook post-halving bull market, with upside scenarios increasingly in focus.

The debate was no longer if Bitcoin would be legitimized that question had already been settled but how that legitimacy would interact with Bitcoin’s market cycle, investor behavior, and long-term adoption path.

The chart below shows how 2025 ultimately unfolded relative to those bear, base, and bull case projections, capturing the defining dynamic of the year: meaningful structural progress alongside a maturing, more complex market cycle.

For readers looking to revisit the framework behind these scenarios, see our full Bitcoin Price Outlook for 2025.

Q1 2025 | Post-election momentum, personnel, and the policy inflection

Bitcoin entered 2025 coming directly off the powerful post-election rally of Q4 2024.

In early January, price briefly pushed back above $100,000, retesting the 2024 all-time high as markets anticipated rapid follow-through from the incoming Trump administration.

What followed instead was a pause and a sell-off.

As the administration began installing key personnel across Treasury, the SEC, and other regulatory bodies, Bitcoin sold off through the quarter. This was not a rejection of Bitcoin, but a familiar market response to political transition risk: uncertainty while new leadership is put in place, priorities clarified, and policy direction formalized.

Two confirmations mattered most during this phase:

Scott Bessent’s confirmation as Treasury Secretary, signaling an explicit shift toward treating Bitcoin as a strategic asset and store of value.

Paul Atkins’ confirmation as SEC Chair, reinforcing expectations of a move away from regulation-by-enforcement toward engagement and market structure clarity.

These appointments laid the groundwork but they were not the catalyst.

That catalyst arrived in March with the announcement of a Strategic Bitcoin Reserve. This marked the first unequivocal policy action translating campaign rhetoric into reality. Bitcoin was no longer merely tolerated it was being explicitly positioned within the national strategic framework.

Q1, in retrospect, was the transition from anticipation to implementation and the sell-off reflected uncertainty before the policy signal, not doubt after it.

Q2 2025 | Post-halving bull market confirmation and industry acceleration

Q2 marked the confirmation phase of the post-halving bull market.

With federal posture clarified and the Strategic Bitcoin Reserve establishing credibility, Bitcoin reversed its Q1 weakness and resumed its uptrend. Price reclaimed key levels and by mid-year, reached the first major bull-market milestone: the zone aligned with our bear-case scenario ($115,000).

This was an important psychological level.

Rather than signaling exhaustion, it reinforced the view that Bitcoin was tracking a historically normal bull-market expansion, supported not by speculation alone but by accelerating adoption across governments, institutions, and corporations.

The dominant theme of Q2 was industry acceleration:

U.S. states moved rapidly to establish Bitcoin reserve frameworks

Institutional asset managers and global sovereign investment increased

Corporate Bitcoin holdings reached new records

Price strength and news flow reinforced one another. Confidence returned. Expectations expanded. The market began looking beyond the bear-case pathway toward higher-end outcomes.

Q3 2025 | Momentum, consolidation, and the setup for new all-time-highs

Bitcoin entered the quarter strong, consolidating after its Q2 advance and maintaining bullish structure. At the same time, legislative momentum continued. The passage of the GENIUS Act marked a meaningful shift in U.S. digital-asset policy, particularly around stablecoins and payments infrastructure. This reinforced the sense that the broader digital-asset ecosystem was being absorbed into the regulatory perimeter.

However, this progress came with a trade-off, narrative dilution.

Q3 marked the rise and peak of Bitcoin treasury companies. Following the playbook pioneered earlier in the cycle, a wave of public companies positioned Bitcoin holdings as their primary value proposition. These vehicles attracted significant attention and capital, particularly from retail investors seeking leveraged or equity-based exposure to Bitcoin’s upside. Valuations expanded quickly, and the “ Treasury company” narrative became a dominant theme across public markets.

At the same time, crypto-native company IPOs accelerated, further broadening digital asset exposure within equity markets. This influx of listings shifted attention away from Bitcoin itself and toward a growing constellation of Bitcoin- and crypto-adjacent equities, increasing complexity and fragmenting investor focus.

Alongside this, the narrative scope widened beyond Bitcoin. Regulatory momentum particularly around payments and market structure reignited interest in stablecoins and tokenized real-world assets, pulling capital and media attention toward the broader digital asset ecosystem. While these developments were constructive for the industry as a whole, they diluted Bitcoin’s singular narrative dominance.

This fragmentation was reflected clearly in Bitcoin’s price behavior. After its strong advance in Q2, Bitcoin spent much of Q3 consolidating at elevated levels, digesting gains rather than extending them. Late in the summer, price made a decisive push higher, briefly threatening a breakout from consolidation and raising expectations for a renewed leg up in the post-halving bull market.

That breakout failed. Rather than signaling renewed momentum, this move proved to be a liquidity event. For long-term Bitcoin holders many sitting on multi-year gains the attempted breakout provided an attractive opportunity to take profits and rebalance portfolios. This selling was not panic-driven, but disciplined and rational, reflecting Bitcoin’s growing role as a macro asset rather than a speculative novelty.

By the end of Q3, Bitcoin had not broken structurally but it had revealed tension beneath the surface. Momentum stalled, narratives multiplied, and distribution quietly increased, setting the stage for the repricing and reckoning that would follow in Q4.

Q4 2025 | The proxy reckoning and cycle reassertion

The failed breakout attempt late in the summer proved consequential. What initially looked like consolidation beneath resistance quickly turned into a rapid reversal, as selling pressure from long-term holders met fading marginal demand. This pattern is familiar in Bitcoin’s history — late-stage cycle moves often fail not because fundamentals deteriorate, but because liquidity has already been pulled forward.

The turning point came in October, when MSCI published its consultation on Digital Asset Treasury (DAT) companies, proposing that firms whose primary activity was holding Bitcoin or other digital assets be classified as fund-like vehicles rather than operating businesses. Under the proposal, companies with digital assets representing a majority of their balance sheets could be excluded from major equity indexes.

This was the structural boundary the market had been ignoring.

The reaction was swift and decisive:

Bitcoin treasury company enthusiasm collapsed

Proxy valuations repriced sharply

Capital rotated away from speculative crypto and back toward fundamentals

At the same time, Bitcoin itself broke key technical levels. The loss of the $100,000 psychological support marked a clear shift in market psychology. Price retraced into the high-$80,000 range by year-end, and familiar questions resurfaced:

Is this time different?

Has the cycle ended?

Is a bear market beginning?

These fears were not new they have appeared at every major Bitcoin transition. What made Q4 different was what did not change. Fundamentals did not deteriorate. Regulation did not tighten. Access did not collapse. Instead, Bitcoin was repriced within a system that had already accepted it.

By the end of 2025, Bitcoin had clearly exited its post-election, post-halving impulse phase. Froth had been flushed. Proxy narratives had been repriced. The cycle had reasserted itself not through collapse, but through normalization.

Historically, cycle peaks have coincided with weakening fundamentals, hostile regulation, and shrinking access. The transition into 2026 looks materially different. Instead of contraction, Bitcoin enters the next phase with clear, measurable tailwinds across regulation, allocation, and real-world integration.

This sets up the defining question for the year ahead:

Is the Bitcoin market cycle ending or evolving into a longer-duration adoption phase?

Looking ahead to 2026

2025 closed the chapter on Bitcoin’s legitimacy debate. 2026 opens the chapter on how Bitcoin is priced once legitimacy is assumed.

That is the focus of our Bitcoin 2026 Price Outlook - Structural growth in a maturing market.